Government policies

UIDAI Mandates Aadhaar Verifier Registration

UIDAI Mandates Aadhaar Verifier Registration | The Unique Identification Authority of India (UIDAI) will shortly notify a rule requiring entities such as hotels, event organisers and other offline verification-seeking businesses to register with the authority before conducting Aadhaar-based identity checks, aiming to curb paper copies of Aadhaar cards and align with the Digital Personal Data Protection Act. Registered entities will be granted access to QR code scanning and integration with the forthcoming Aadhaar app or API, facilitating paperless offline verification and reducing dependency on central server authentication. The mandate is designed to discourage contravention of the Aadhaar Act through physical storage of Aadhaar data and enhance privacy safeguards for individuals. Non-registered entities will be unable to perform Aadhaar verification under the new framework once it takes effect. Notification is pending formal promulgation by UIDAI. (Economic Times)

Mexico Raises Tariffs on Indian Exports

Mexico Raises Tariffs on Indian Exports | Mexico’s Senate has approved a substantial tariff overhaul that will impose duties of up to 50% on imports from countries without a Free Trade Agreement with Mexico, including India, with the higher levies expected to take effect in 2026 and sharply raise duties on passenger vehicles and auto parts from the current 20% level. This change will directly impact Indian automotive exports worth around $1 billion to Mexico, where major manufacturers such as Volkswagen, Hyundai, Nissan and Maruti Suzuki currently ship vehicles, potentially reducing price competitiveness and export volumes. The tariff regime applies to more than 1,400 product categories and aims to protect domestic industries and strengthen Mexico’s fiscal position. Higher duties could compel Indian automakers to reassess supply chain and market strategies for Latin America, and may prompt engagement between Indian trade authorities and Mexico. (Reuters)

India Eases FDI and Regulatory Processes

India Eases FDI and Regulatory Processes | The Government of India has raised the foreign direct investment (FDI) limit in the insurance sector from 74% to 100% for companies investing the entirety of premiums within India, as announced in the Union Budget 2025-26, with an associated review of conditionalities and guardrails to be simplified. In addition, the budget outlines plans to set up a forum for regulatory coordination and pension product development, roll out a revamped Central KYC Registry in 2025 to streamline periodic updates, and rationalise procedures for speedy approval of company mergers, including broadening fast-track merger processes. The reforms aim to boost foreign investment attractiveness, expand financial sector depth, and reduce compliance frictions for businesses. The policy measures are part of a broader strategy to enhance global competitiveness and foster a business-friendly regulatory environment. (Press Information Bureau)

Goods and services tax

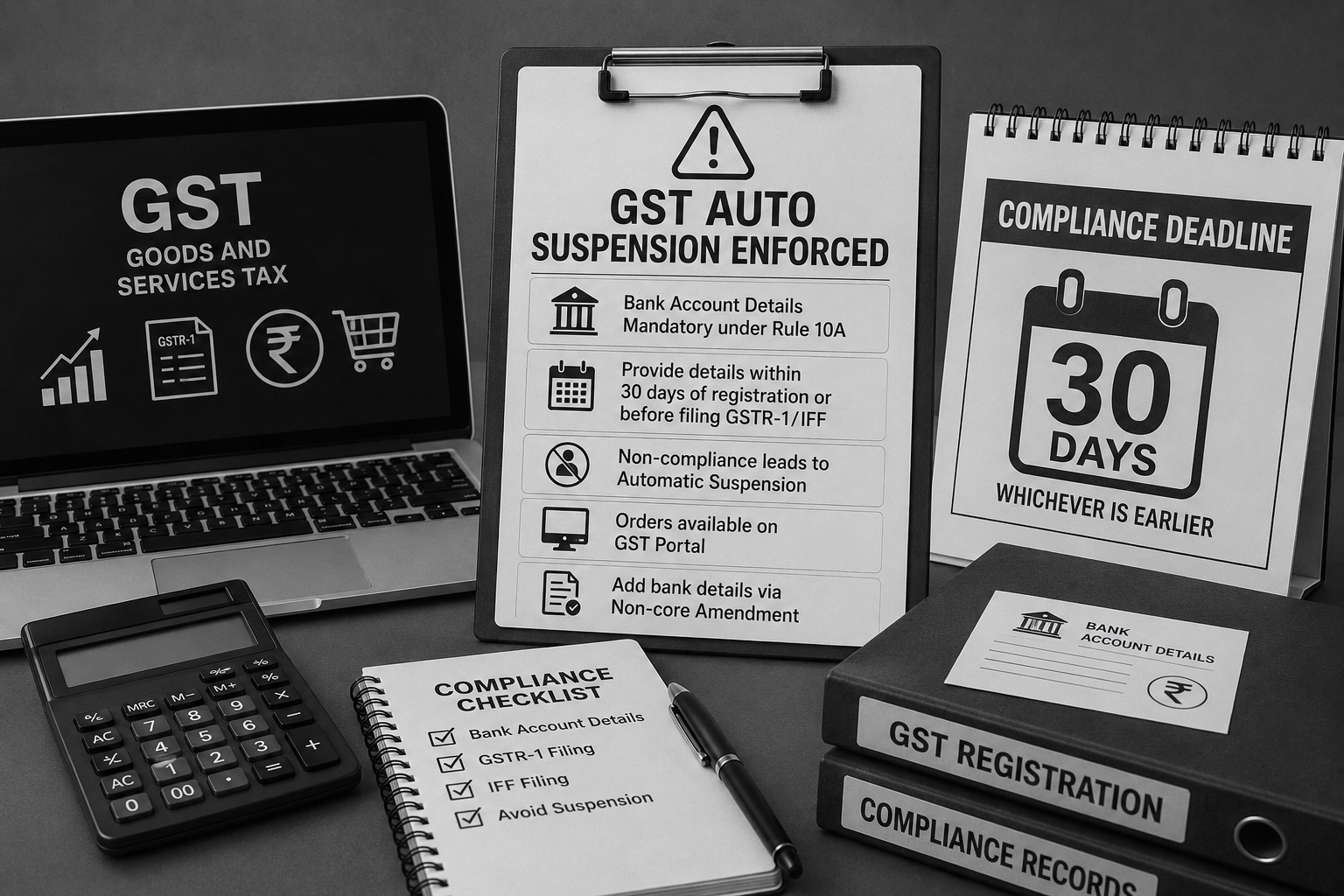

GST Auto Suspension Enforced

GST Auto Suspension Enforced | The Goods and Services Tax Network has implemented system-driven auto suspension of GST registrations for non-furnishing of bank account details under Rule 10A, as notified on December 5, 2025. Regular taxpayers, excluding TCS, TDS and suo motu registrations, must provide bank details within 30 days of grant of registration or before filing GSTR-1 or IFF, whichever is earlier. Failure to comply triggers automatic suspension, with orders accessible on the GST Portal under View Notices and Orders. Bank details can be added through a non-core amendment, after which cancellation proceedings are designed to be auto-dropped, with a manual drop option available if not processed the same day. OIDAR and NRTP taxpayers are generally exempt, except OIDAR registrants appointing an Indian representative, for whom bank details are mandatory, creating immediate compliance risk for new businesses. (Goods and Services Tax Network)

Income Tax

Direct Tax Collections Climb 8%

Direct Tax Collections Climb 8% | India’s net direct tax collections in the current financial year (FY26) rose by 8% to approximately ₹17.04 lakh crore up to December 17, 2025, driven largely by higher corporate advance tax payments and steady compliance, according to provisional data from the Income Tax Department. Gross collections before refunds were about ₹20.01 lakh crore, while refund outflows declined 13.5% to ₹2.97 lakh crore, supporting the net growth. Corporate tax receipts were a major contributor, with corporate advance tax up around 8%, although advance tax from non-corporate taxpayers dipped during the period. Net collections from non-corporate sources, including personal income tax and STT, also showed solid year-on-year gains. The figures suggest the government is on course toward its FY26 direct tax target of ₹25.2 lakh crore amid controlled refund disbursements and resilient business earnings. (Economic Times)

Corporate and allied laws

MCA Raises Small Company Thresholds

MCA Raises Small Company Thresholds | The Ministry of Corporate Affairs has amended the Companies (Specification of Definition Details) Rules, 2014 via Notification G.S.R. 880(E) effective December 1, 2025, revising the definition of a “small company” under Section 2(85) of the Companies Act, 2013. Under the new rules, a private company (other than a public company) will qualify as a small company if its paid-up share capital does not exceed ₹10 crore and its turnover in the preceding financial year does not exceed ₹100 crore, up from the prior limits of ₹4 crore and ₹40 crore respectively. Companies meeting these thresholds can continue to avail compliance relaxations such as simplified financial reporting, reduced board meeting requirements, and lower penalties for defaults. The expanded eligibility is expected to bring more startups and MSMEs under the simplified regulatory regime, easing governance and compliance costs. Exclusions remain for holding companies, subsidiaries, Section 8 companies, and entities governed by special Acts. (Business Standard)

SEBI Tightens SME IPO Profit Criteria

SEBI Tightens SME IPO Profit Criteria | The Securities and Exchange Board of India has introduced a new ₹1 crore EBITDA profitability test for companies seeking to list on the SME IPO platform under the ICDR Regulations, effective from the March 2025 amendment. Firms must demonstrate operating profit (EBITDA) of at least ₹1 crore in two of the last three financial years before filing their Draft Red Herring Prospectus, aiming to improve IPO quality and investor assessment. This replaces looser profitability norms and is designed to discourage speculative listings lacking consistent earnings, especially where operating losses are frequent. The rule directly affects eligibility for capital raising via SME listings and requires robust financial performance evidence at the time of IPO filing. (Economic Times)

SEBI Revises REIT Investor Definitions

SEBI Revises REIT Investor Definitions | SEBI has updated the REIT Regulations to broaden the definition of institutional and strategic investors, enabling wider participation in real estate investment trusts and infrastructure investment trusts. The amendments focus on expanding eligible categories, including entities that meet Qualified Institutional Buyer criteria, and clarifying investor roles in public offerings. Minimum investment thresholds such as strategic investors jointly or individually investing at least 5 % of the offer size have been codified to support deeper institutional engagement and market development. These changes are intended to align REIT investor definitions with broader capital market norms and enhance governance clarity. (Financial Express)

Finance & Banking

Supreme Court Defines NI Act Jurisdiction

SC Defines NI Act Jurisdiction | The Supreme Court of India has clarified territorial jurisdiction in cheque dishonour prosecutions under Section 138 of the Negotiable Instruments Act, 1881 with effect from the 2015 amendment, holding that only the court within whose local limits the payee’s home-branch bank (where the account is maintained) is situated has jurisdiction to try such cases, ending prior forum-shopping confusion. This interpretation reinforces the statutory language of Section 142(2)(a) and emphasises the need to correctly identify the branch location for complaint filing. Courts cannot dismiss or transfer cases based on erroneous jurisdiction once evidence under Section 145 has commenced. The ruling has procedural implications for litigants and advocates handling cheque bounce litigation across multiple jurisdictions. (Economic Times)

RBI Withdraws 9,445 Circulars

RBI Withdraws 9,445 Circulars | The Reserve Bank of India has consolidated its regulatory framework by issuing 244 function-wise Master Directions for regulated entities and formally withdrawing 9,445 legacy circulars, guidelines and directions that were identified as obsolete or redundant, effective following notifications in late November 2025. The consolidation covers multiple sectors including commercial banks, NBFCs, co-operative banks and payment banks, creating a single, cohesive regulatory reference library to reduce cross-referencing and compliance ambiguity. Withdrawn circulars will no longer be treated as standalone sources, though actions started under them remain governed by previous instructions where applicable. The Master Directions were finalised after public consultation and are expected to enhance regulatory clarity and operational efficiency. (Economic Times)

RBI Mandates LRS Daily Returns

RBI Mandates LRS Daily Returns | The Reserve Bank of India has issued A.P. (DIR Series) Circular No. 17 dated December 3, 2025, directing that Authorised Dealer (AD) Category-II banks/entities and Full-Fledged Money Changers (FFMCs) must submit Liberalised Remittance Scheme (LRS) daily returns directly on the Centralised Information Management System (CIMS) from January 1, 2026. Previously only AD Category-I banks filed these returns on behalf of attached Category-II entities and FFMCs. Direct submission, including nil reports, will enable real-time PAN-wise monitoring of cumulative LRS remittances before further transactions are approved. This change updates the Master Direction on FEMA reporting and aims to strengthen compliance and limit-tracking across authorised foreign exchange dealers. (Money Control)

RBI Governor Highlights Economic Trends

RBI Governor Highlights Economic Trends | In the Governor’s Statement dated December 5, 2025, the Reserve Bank of India noted robust GDP growth and benign inflation, with headline inflation averaging below the lower tolerance threshold of the RBI’s target range in Q2 2025-26 and real GDP expansion supported by consumer spending and GST rate rationalisation. The statement reflects the central bank’s assessment of macroeconomic developments and its regulatory stance heading into 2026, emphasising sustained financial system consolidation and ongoing refinement of regulatory frameworks to support ease of doing business and financial stability. (Press Information Bureau)

Customs & Foreign Trade

DGFT Streamlines IEC Application Process

DGFT Streamlines IEC Application Process | The Directorate General of Foreign Trade amended Paragraph 2.08 of the Handbook of Procedures via Public Notice No. 32/2025-26 dated November 20, 2025, merging ANF-1A into a revised ANF-2A to simplify Importer-Exporter Code (IEC) applications. Under the revised framework, ANF-1A is discontinued and all IEC issuance, modification and related filings must use the updated ANF-2A with online system-based electronic verification of applicant details through integrated government databases, reducing manual validation. Applicants must continue to provide essential documents unless the digital system grants exemptions, and post-verification guidelines will be issued by DGFT Headquarters. Paras 2.08(c)(i) and 2.08(c)(ii) remain unchanged, maintaining key procedural requirements. The change formalises a fully electronic, paperless IEC process, improving accuracy and turnaround times for trade compliance. (Taxscan)

CBIC Launches Fully Digital SWIFT 2.0 Platform

CBIC Launches Fully Digital SWIFT 2.0 Platform | The Central Board of Indirect Taxes and Customs issued Circular No. 29/2025-Customs on November 21, 2025, announcing SWIFT 2.0, an upgraded Single Window Interface for Facilitating Trade to serve as a unified digital touch point for importers, exporters, customs brokers and Partner Government Agencies (PGAs) for EXIM processes. SWIFT 2.0 replaces the legacy repository model, enabling online submission of additional data and documents for NOC processing, real-time tracking via dashboards, SMS/email alerts, and online payment of PGA fees with digital NOC access. The first phase mandates onboarding of Animal Quarantine and Certification Services (AQCS), Plant Quarantine Management System (PQMS) and FSSAI from December 1, 2025, with phased integration of 60+ PGAs. Importers and exporters must file requisite details through Integrated Declaration in the Bill of Entry or the unified application dashboard to ensure compliance. Field formations are directed to issue trade notices to ensure accurate filings and smooth transition to the fully digitised platform. (Taxscan)

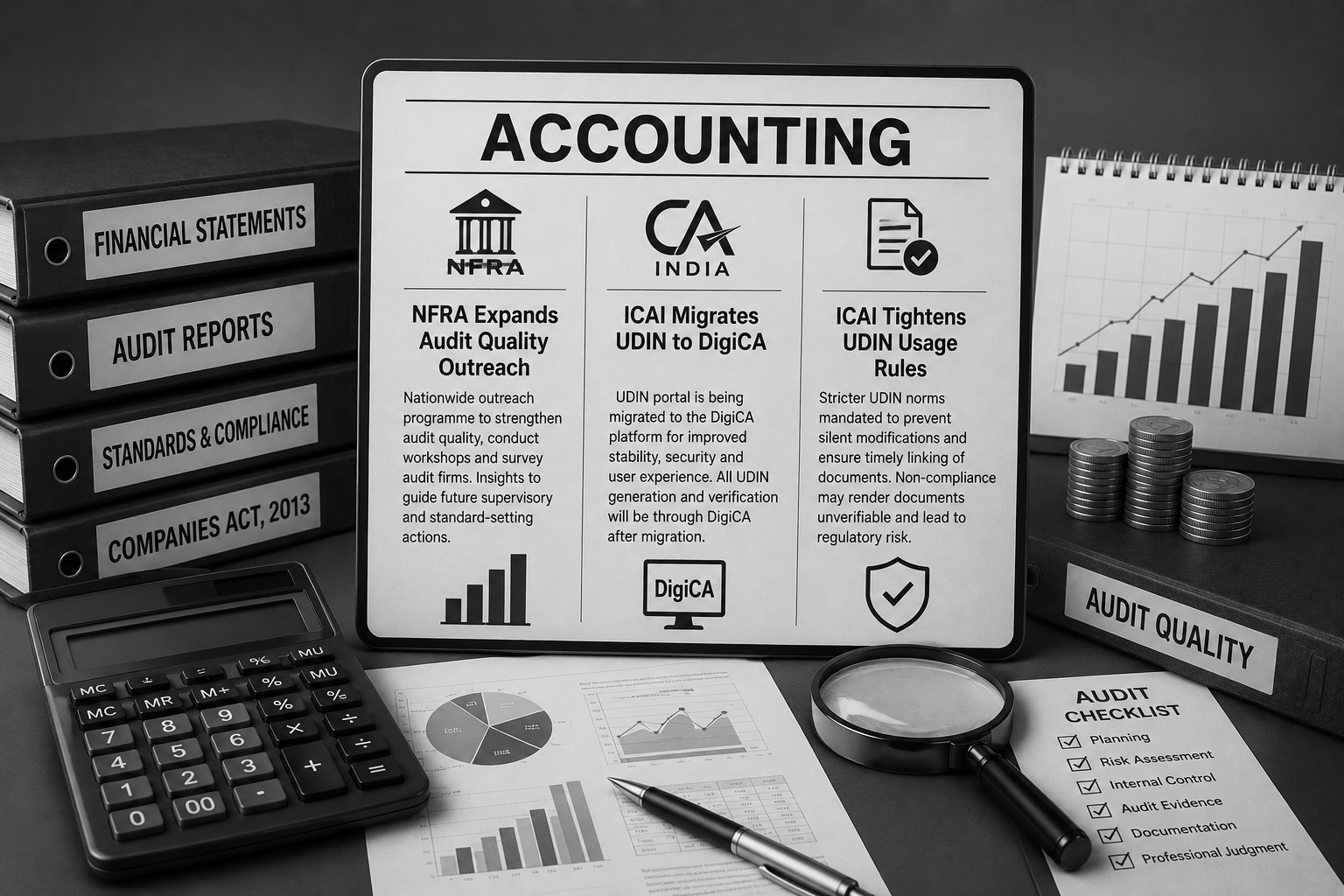

Accounting

NFRA Expands Audit Quality Outreach

NFRA Expands Audit Quality Outreach | The National Financial Reporting Authority has rolled out a nationwide outreach programme to strengthen audit quality and compliance standards across audit firms, including small and mid-sized practices. The initiative involves regional workshops, direct engagement with auditors, and a nationwide audit firms survey to gather data on audit practices, capacity and challenges. NFRA has indicated that insights from the outreach and survey will guide future supervisory, inspection and standard-setting actions under the Companies Act framework. The programme focuses on improving consistency in audit execution, documentation and professional judgement. For audit firms and companies, this signals closer regulatory engagement and a sharper focus on audit quality benchmarks. (Economic Times)

ICAI Migrates UDIN to DigiCA

ICAI Migrates UDIN to DigiCA | The Institute of Chartered Accountants of India has announced the migration of the Unique Document Identification Number portal to the DigiCA digital platform to enhance system stability, security and user experience. The transition involves a temporary downtime during the migration window, after which all UDIN generation and verification will be routed exclusively through DigiCA. ICAI has advised members to plan certificate and report issuance accordingly to avoid compliance delays. The upgraded platform is intended to support higher transaction volumes and improved audit trail features. For chartered accountants and regulated entities, timely adaptation is essential to ensure uninterrupted statutory filings. (Financial Express)

ICAI Tightens UDIN Usage Rules

ICAI Tightens UDIN Usage Rules | The Institute of Chartered Accountants of India has released a detailed UDIN portal manual mandating stricter usage norms to eliminate silent modifications in certified documents. The updated guidance requires UDIN generation for a wider set of attestations and reinforces timelines for linking UDINs with documents issued by members. Non-compliance may render documents unverifiable on the ICAI system, increasing regulatory and client risk. The manual also outlines enhanced verification checks available to regulators and stakeholders. Businesses relying on certified financial and compliance documents may face delays or re-issuance if UDIN requirements are not strictly followed. (Business Standard)

Payroll & Personal Finance

PFRDA Expands NPS Equity Options

PFRDA Expands NPS Equity Options | The Pension Fund Regulatory and Development Authority has introduced two new high-equity auto investment choices for Central Government National Pension System subscribers, increasing total lifecycle options from four to six. The new options allow equity exposure of up to 75% during early service years, with a structured tapering as the subscriber approaches retirement age. The change was notified through an official circular following amendments approved by the Ministry of Finance. Subscribers opting out of the default scheme must actively select a pension fund and lifecycle option through the CRA system. The move provides greater long-term return potential but also increases market-linked risk exposure for government employees. (ET Wealth)

RBI Caps Currency Carry to Nepal & Bhutan

RBI Caps Currency Carry to Nepal, Bhutan | The Reserve Bank of India has revised limits on Indian currency that residents may carry while travelling to Nepal and Bhutan to curb misuse of high-value notes. As per updated directions, travellers may carry Indian currency notes up to ₹25,000, excluding denominations of ₹500 and ₹2,000. The restriction applies to both leisure and business travel and aligns with existing foreign exchange regulations. Authorised dealers and banks are required to ensure compliance while facilitating travel-related forex services. Businesses sending employees on cross-border travel must align internal travel policies with the revised limits. (Financial Express)

NPS Exit Framework Definitions Revised

NPS Exit Framework Definitions Revised | The Pension Fund Regulatory and Development Authority has revised the National Pension System exit and withdrawal framework to introduce uniform definitions across regulations. The update standardises terminology for superannuation, premature exit, partial withdrawal and annuity purchase to remove interpretational ambiguity. The revised framework applies across all NPS sectors, including corporate and government subscribers. Points of Presence and intermediaries must update internal processes and subscriber communication accordingly. The clarification improves operational consistency and reduces disputes during exit and settlement processing. (Economic Times)

Table of Contents

FAQ's

The main benefit is better stability. Wi-Fi 7 helps homes manage many connected devices at the same time with less congestion, lower delay, and fewer connection drops.

No. Wi-Fi 7 can offer higher speeds, but its bigger value for smart homes is responsiveness. It helps cameras, doorbells, smart speakers, TVs, and other devices work more smoothly together.

No. Basic devices like smart bulbs, plugs, and sensors may not need Wi-Fi 7 directly. But they can still benefit from a better overall network when heavy devices like TVs, laptops, and cameras are handled more efficiently.

It can help, especially if the problem is caused by Wi-Fi congestion or weak network performance. However, router placement, internet plan quality, device support, and home layout also matter.

You should consider it if your home has many connected devices, smart cameras, video doorbells, multiple streaming devices, gaming consoles, or work-from-home setups. For smaller homes with basic usage, Wi-Fi 6 may still be enough.