PE Risk Assessment

Evaluating taxable presence exposure in India under domestic law and tax treaty India provisions.

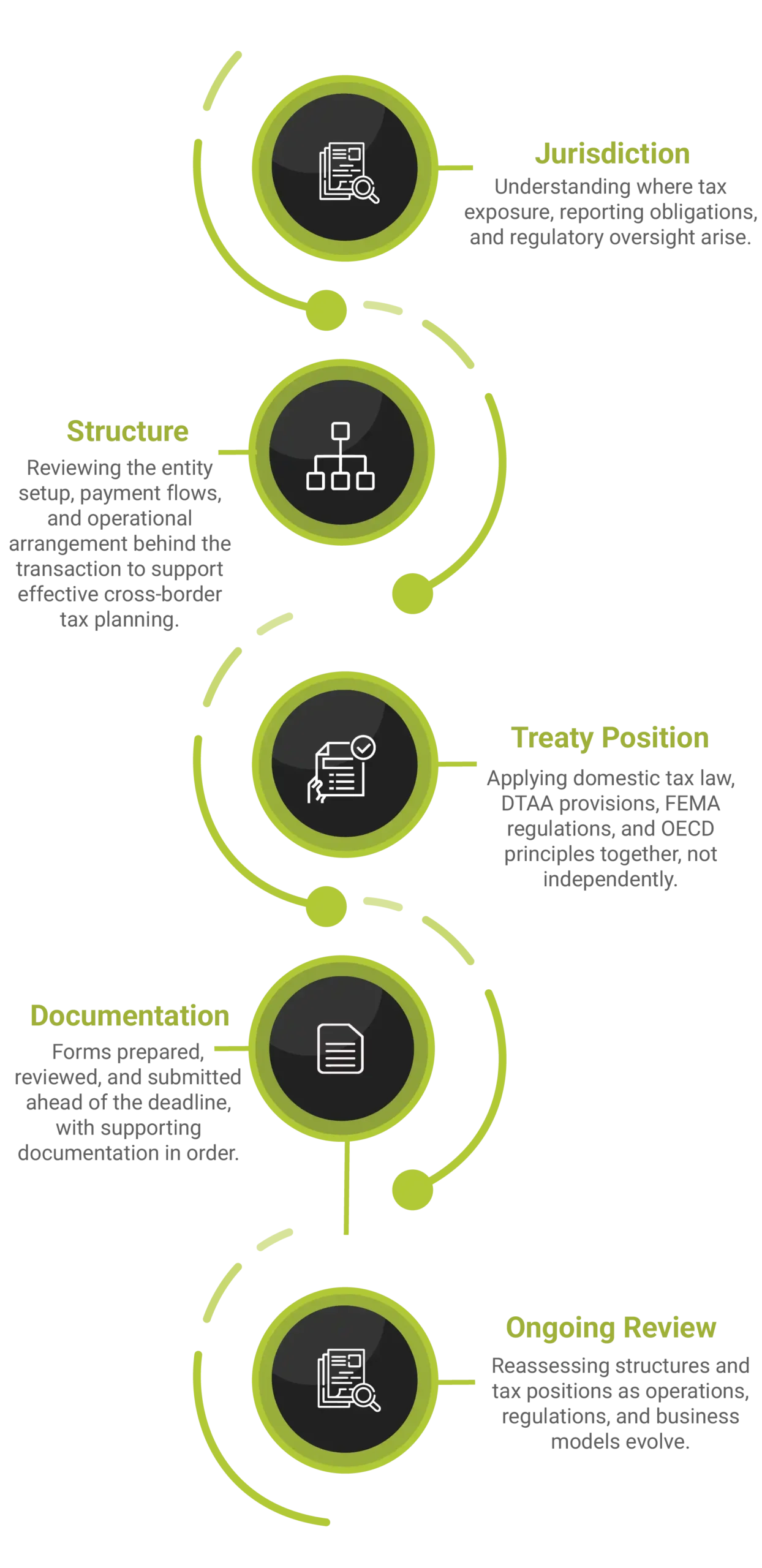

Business Structuring

Managing India tax on repatriation of profits, royalties, dividends, and service fees for businesses.

Tax Repatriation

Managing repatriation of royalties, dividends, fees, and profits.

Advance Rulings

Obtaining clarity on tax treatment before transactions are executed.

ITR & Assessments

Tax filing and assessment support for foreign entities operating in India.

")

Withholding Tax Advisory

Determining withholding tax obligations in India on payments made to non-residents.

Foreign Tax Credits

Evaluating and claiming eligible foreign tax relief in India, including applicable DTAA benefits where available.

Inter-Company Agreements

Drafting cross-border agreements aligned with transfer pricing principles.

Cross-Border Documentation

Maintaining transaction documentation aligned across jurisdictions.

Treaty Position Review

Reviewing DTAA applicability and cross-border tax exposure.